The Veterans Affairs home loans are unique mortgage options that allow current and former members of the military to own a piece of the American dream by potentially qualifying for homes that they might have thought to be out of reach.

Veterans, active-duty service personnel, and select Reservists or National Guard members are among those who can qualify for VA loans. These flexible loans come with outstanding benefits like no down payment, no mortgage insurance, more lenient credit requirements, and also have the lowest average interest rates on the market.

The National Association of Realtors (NAR) 2017 Profile of Home Buyers and Sellers showed that 18 percent of recent home buyers are veterans, while three percent are active-duty service members.

However, misinformation and misconceptions about VA loans continue to hinder many veterans from actually benefiting from this program, which is a tangible way of showing gratitude towards their service to the people and the nation.

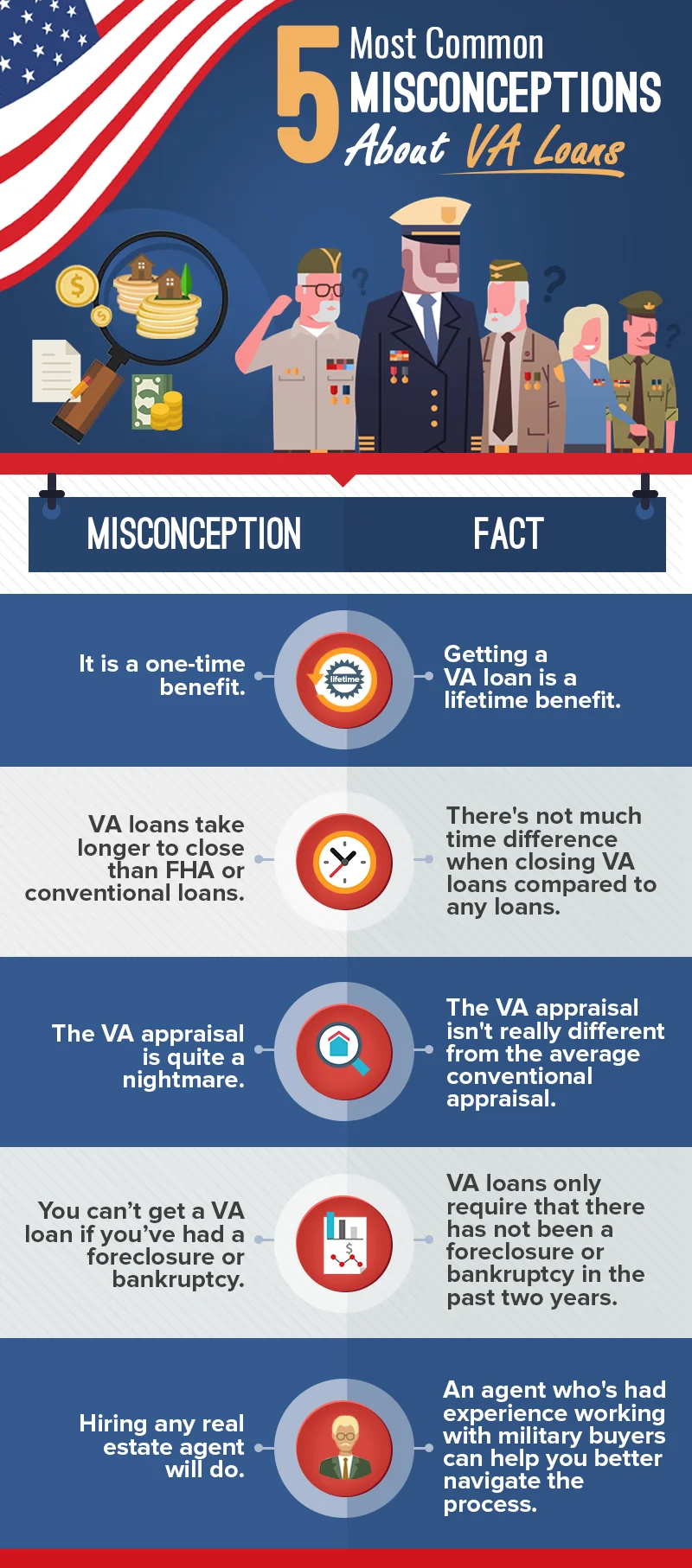

#1 Misconception: It is a one-time benefit.

FACT: Getting a VA loan is a lifetime benefit.

Some veterans think that they must use the benefit immediately or lose it, or that if they used it once, they can’t use it again. The reality is that it is a lifetime benefit. You can use it again to purchase another property, as long as you have paid off your previous VA loan.

#2 Misconception: VA loans take longer to close than FHA or conventional loans.

FACT: There's not much time difference when closing VA loans compared to any loans.

Many home buyers think that VA loans take more than 60 days to close, but it certainly isn't true. The process has become much more automated and efficient with the Guaranty Program, and it can now be closed in 30 days or less.

Similarly, the average VA mortgage closes in 45 days, according to mortgage industry analysts Ellie Mae. While the average closing time for all loans is 42 days, which only has a three-day difference.

#3 Misconception: The VA appraisal is quite a nightmare.

FACT: The VA appraisal isn't really different from the average conventional appraisal.

Unless the buyer pursues a home in a very poor condition, then the appraisal process could really be terrible. The truth is that only VA-approved appraisers inspect the homes to make sure they meet minimum property requirements, and to make sure that they are “safe, sound and sanitary.” VA appraisers also tend to have stricter standards than a typical home appraiser. Otherwise, if the service member chooses a home that is in good condition, then the VA appraisal will be a breeze.

#4 Misconception: You can’t get a VA loan if you’ve had a foreclosure or bankruptcy.

FACT: VA loans only require that there has not been a foreclosure or bankruptcy in the past two years.

VA loans are more lenient than other loan products when it comes to bankruptcy and foreclosure. In some cases, it is also possible to get a loan within a year. This is a much shorter period compared to what FHA loans and conventional mortgages require, which includes a 3-year waiting period.

#5 Misconception: Hiring any real estate agent will do.

FACT: An agent who's had experience working with military buyers can help you better navigate the process.

While any realtor can technically help you, finding a military-friendly real estate agent who particularly had experienced working with military buyers before — and have the time to focus on your needs — can make a world of difference. For many veterans, housing needs go far beyond the usual housing criteria, such as the number of bedrooms, price range and location. An agent who specializes in VA loans can help save you an awful lot of headaches as they better understand the loan process, the VA appraisal, and has a special eye and heart towards your specific situation.